The biggest story in cannabis in 2025 wasn’t a new state market, a major merger or a regulatory overhaul. It was a product category that many once treated as secondary, an afterthought.

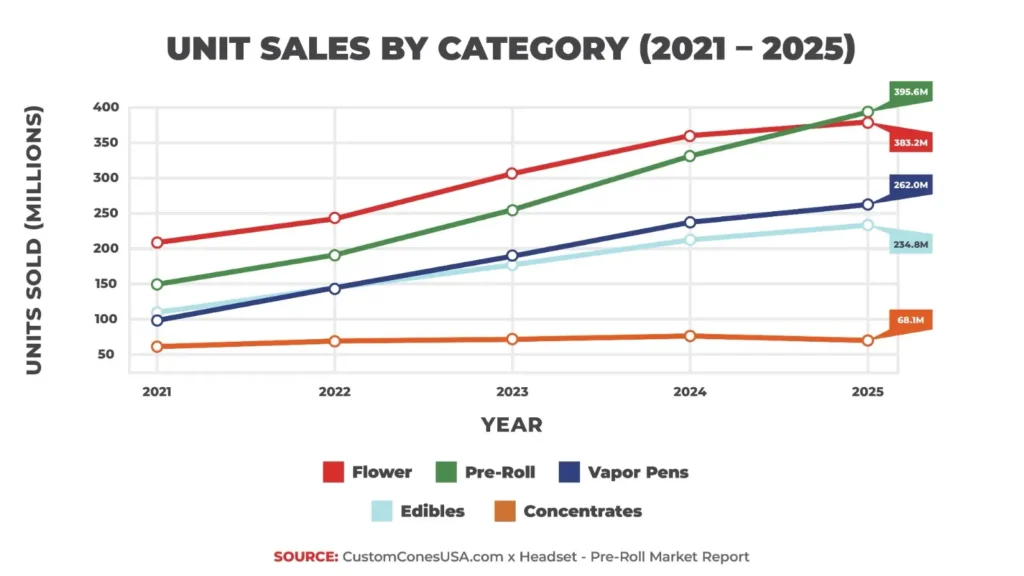

But according to Custom Cones USA’s 2026 State of the Pre-Roll Market Report, pre-rolls overtook flower in unit sales for the first time in history in 2025, making them the top-selling cannabis product on the market by volume. The pre-roll category generated nearly $3.6 billion in revenue, up 9.8% year-over-year, while unit sales rose 18.6% to 383.2 million units. Meanwhile, the overall U.S. cannabis market grew just 1.5%.

That makes pre-rolls not only the top-selling product by units, but also the fastest-growing major category in cannabis.

So why did this happen?

Why Consumers Are Choosing Pre-Rolls

The simplest answer is that pre-rolls now fit the way modern consumers want to shop and, well, consume: they are convenient, intuitive, portable and accessible. In a mature market where convenience often beats ritual, pre-rolls offer a ready-made solution that flower does not. There is no need to grind, , or prepare anything, consumers can walk into a dispensary, buy a product and use it as intended with minimal effort.

That ease of use has become increasingly important as cannabis attracts a wider audience. Longtime enthusiasts may still enjoy the ritual of grinding flower and rolling their own joints and blunts, but mainstream consumers often prioritize speed and consistency. Pre-rolls meet both needs.

Another major factor is product diversity. The pre-roll category today is far more advanced than it was even a few years ago. Consumers can now choose from classic singles, mini pre-rolls, premium glass-tip options, blunt-style products, infused offerings and an expanding array of multi-pack formats. This has allowed the category to move beyond the image of a disposable add-on and become a core area of innovation.

Infused pre-rolls have been especially important. In 2025, they generated $1.68 billion in revenue and accounted for 47% of the category’s total sales dollars. Their unit sales rose 27.8% year-over-year, indicating that many consumers are willing to pay more for a stronger, more flavorful experience.

That premium lane matters because it shows the category is not just growing through low-price convenience, it is also growing through premiumization.

At the same time, value has remained a strength. The average pre-roll price dropped to $9.31 in 2025, down 6.6% from 2024 and nearly 20% from the 2022 peak. Consumers looking to control spending may see pre-rolls as a manageable purchase compared to larger flower buys.

Multi-packs add another layer to the value proposition. Nearly half of all pre-roll SKUs in 2025 were multi-packs, and 90 of the top 100 products sold were multi-packs. The 2.5-gram 5-pack emerged as the standout format, generating $612 million in revenue. These products appeal to consumers who want a better price-per-preroll, more convenience and fewer dispensary trips.

The category’s strength is also visible across geographies. California remained the largest pre-roll market by revenue, while Michigan led in volume. New York, however, posted the fastest year-over-year growth at 96% in revenue and 120.4% in units sold, proving the category’s appeal extends from legacy cannabis states to newer adult-use markets.

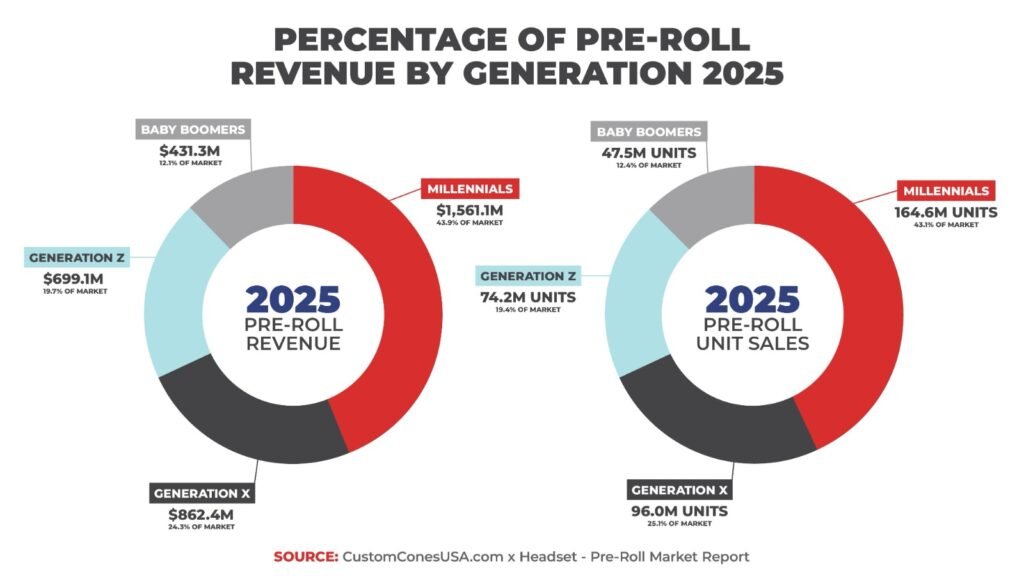

Consumer data points to another reason pre-rolls are outperforming: they appeal to multiple generations. Millennials dominate the category, accounting for 43.9% of revenue, but pre-roll sales grew across every demographic in 2025. Gen Z posted the fastest revenue growth among younger cohorts, while Boomers saw the strongest increase in unit sales. That kind of broad adoption is rare and suggests the category has moved beyond a niche buyer base.

From the business side, producers appear to recognize where things are heading. More than 73% of surveyed operators said they plan to expand their pre-roll product lines, and many are adding multi-packs, lower price-point products, more sizes and infused offerings.

See also: Easy Ways to Get Cannabis

Growth Creates New Competition

Of course, the category is not without risk. Price compression, oversupply and competition are becoming major concerns. More than half of surveyed operators cited the race to the bottom in pricing as the biggest threat to pre-rolls.

But even with those headwinds, the overall direction is unmistakable. Pre-rolls have become the product format that best reflects where cannabis retail is going: simpler, more consumer-friendly and more segmented by occasion and price point.

Flower helped build the legal market. Pre-rolls are helping modernize it. That is why the category did not just grow in 2025, it led.